Available indicators suggest that economic activity has been expanding at a moderate pace. Job gains have slowed this year, and the unemployment rate has edged up through September. More recent indicators are consistent with these developments. Inflation has moved up since earlier in the year and remains somewhat elevated. The Committee seeks to achieve maximum

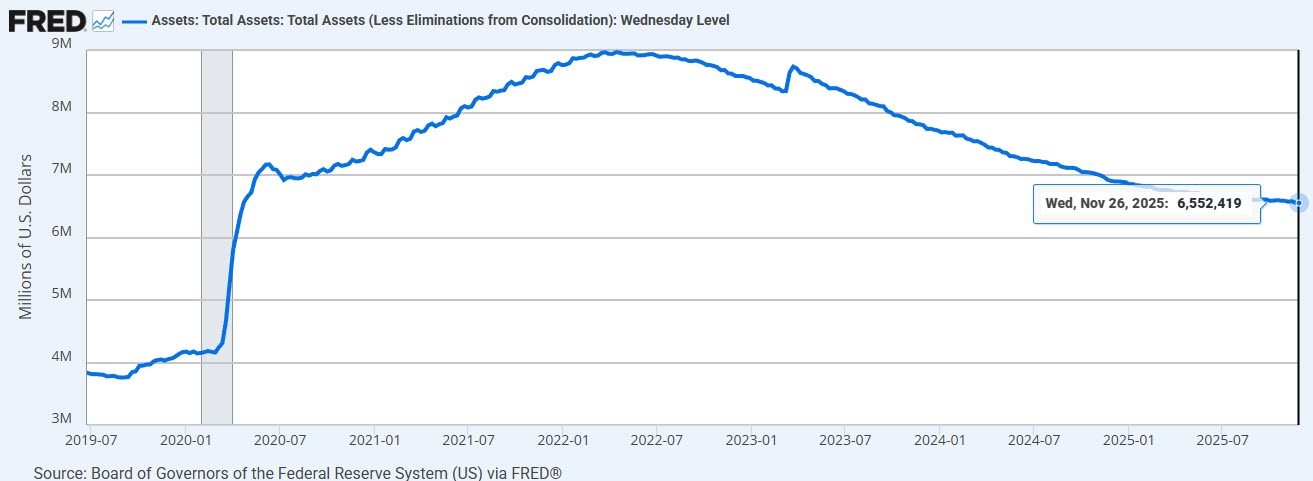

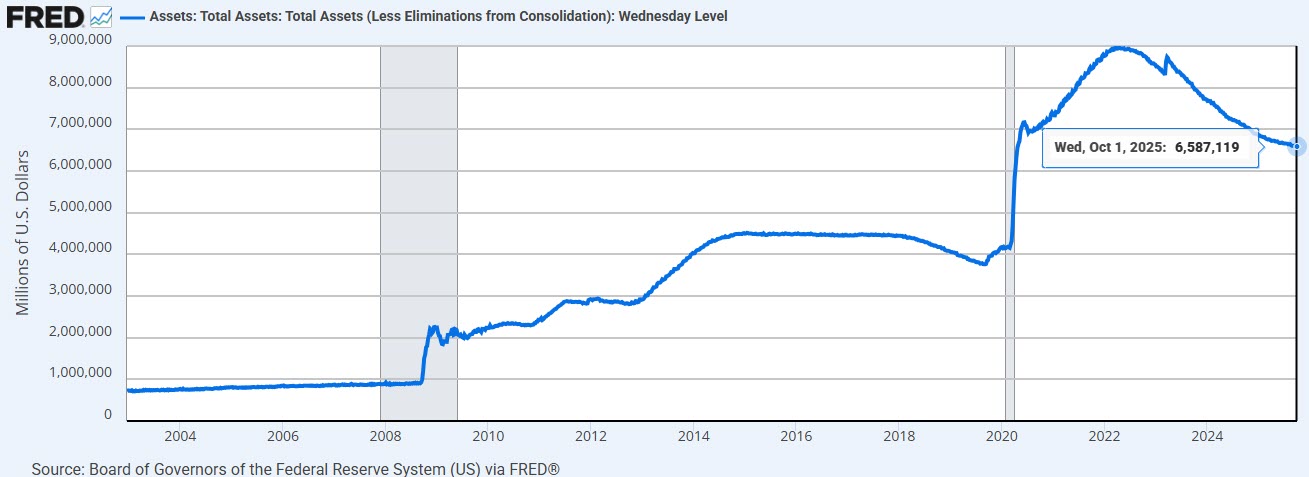

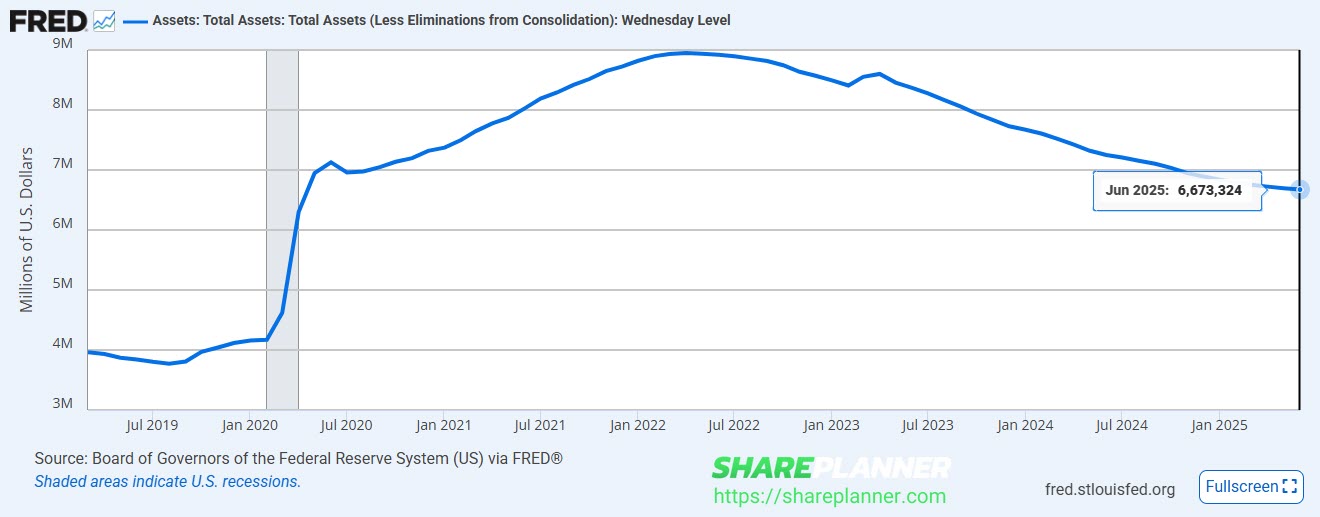

With quantitative tapering (QT) over, we managed to get $2.5T off of the balance sheet, but over $2.5T remains from the rapid increase brought about from Covid.

-

Available indicators suggest that economic activity has been expanding at a moderate pace. Job gains have slowed this year, and the unemployment rate has edged up but remained low through August; more recent indicators are consistent with these developments. Inflation has moved up since earlier in the year and remains somewhat elevated.

The Fed is still very much uninterested in fighting inflation...If they were, their balance sheet wouldn't still be so astronomically high.

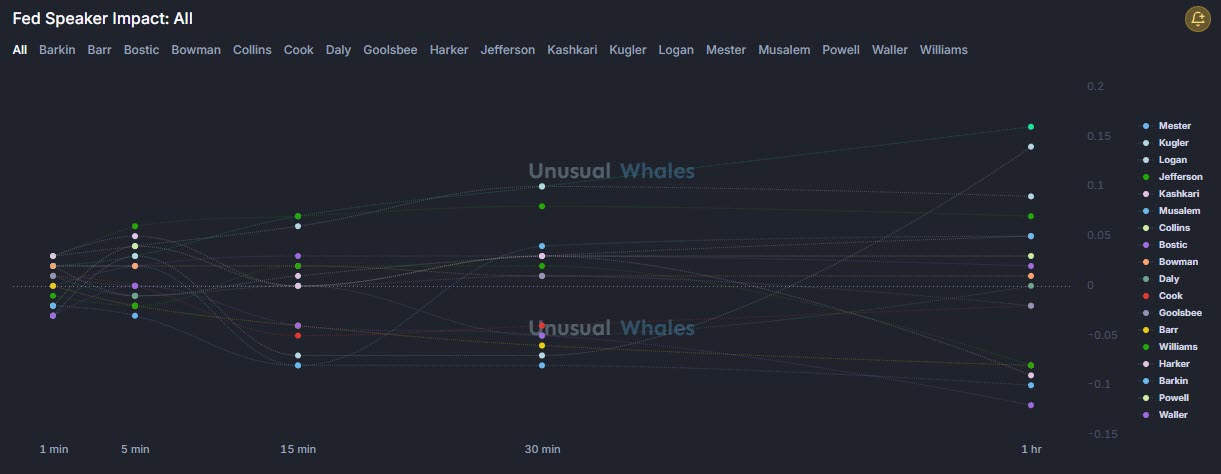

According to the facts here, Loretta Mester is the most bullish while Jerome Powell and Christopher Waller are the most bearish.

Recent indicators suggest that growth of economic activity moderated in the first half of the year. Job gains have slowed, and the unemployment rate has edged up but remains low. Inflation has moved up and remains somewhat elevated.

According to the CME Group, odds for a rate cut over the last week has jump to 98% likelihood.

Fed allowed another $30B to run off its balance sheet this month.

Although swings in net exports continue to affect the data, recent indicators suggest that growth of economic activity moderated in the first half of the year. The unemployment rate remains low, and labor market conditions remain solid. Inflation remains somewhat elevated.

The Fed essentially let 0.4% ($27b) of the balance sheet run off last month. That's not going to make much of a dent.

spc@shareplanner.com

(904) 800-8420

© Copyright 2025 | SharePlanner Inc. All Rights Reserved.

Disclaimer: The information provided on this website is for educational and informational purposes only. Ryan Mallory and/or SharePlanner are not licensed financial advisors, brokers, or tax professionals. The content on this site should not be considered as financial, investment, tax, or legal advice.

All information and opinions expressed herein are based on sources believed to be accurate and reliable. However, we make no representation or warranty as to their accuracy, completeness, or reliability. Any action you take upon the information on this website is strictly at your own risk.

Past performance is not indicative of future results. Investing involves risk, including the possible loss of principal. All investors should make their own decisions based on their specific investment objectives and financial circumstances.

This site may contain links to external websites that are not provided or maintained by or in any way affiliated with Ryan Mallory and/or SharePlanner. Please note that Ryan Mallory and/or SharePlanner do not guarantee the accuracy, relevance, timeliness, or completeness of any information on these external websites.

By using this website, you agree that Ryan Mallory and/or SharePlanner and any affiliated parties are not responsible for any losses or damages resulting from your use of or reliance on the information provided.

It is strongly recommended that you consult with a qualified professional before making any financial decisions.